Percutaneous Coronary Intervention Market Overview

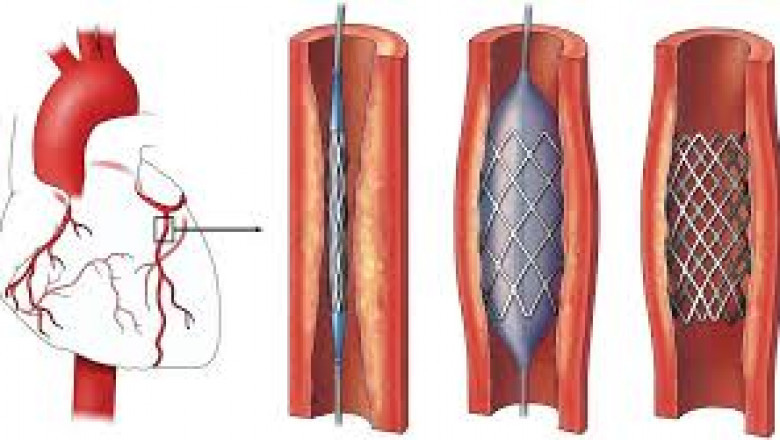

The Percutaneous Coronary Intervention (PCI) market is witnessing significant growth globally, driven by the rising incidence of cardiovascular diseases, an aging population, and continuous advancements in interventional cardiology. PCI, commonly known as coronary angioplasty, is a non-surgical procedure used to treat narrowing of the coronary arteries of the heart found in coronary artery disease. It has become a standard treatment for patients suffering from acute coronary syndromes and stable angina. This minimally invasive technique, which involves the use of a catheter to place a stent to open up blood vessels in the heart, is increasingly preferred over traditional surgical methods due to shorter recovery times and fewer complications. Percutaneous Coronary Intervention Market Industry is expected to grow from 12.87 (USD Billion) in 2025 to 30.43 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 10.03% during the forecast period (2025 - 2034).

The global PCI market is experiencing steady expansion owing to increased healthcare awareness and enhanced accessibility to advanced medical infrastructure. The shift towards value-based healthcare, growth in healthcare expenditure, and a growing preference for minimally invasive procedures are contributing significantly to market growth. Furthermore, the rising prevalence of risk factors such as diabetes, obesity, hypertension, and smoking-related cardiovascular complications further fuels the demand for PCI procedures. Technological innovations such as drug-eluting stents (DES), bioresorbable vascular scaffolds, and intravascular imaging have also positively impacted procedural outcomes, thus attracting wider adoption among healthcare providers.

Key Market Segments

The Percutaneous Coronary Intervention market can be broadly segmented based on device type, procedure type, end-user, and geography.

By device type, the market includes stents, catheters, guidewires, balloons, and others. Among these, stents—particularly drug-eluting stents—dominate the segment due to their effectiveness in reducing restenosis and improving long-term outcomes. Bare-metal stents and bioresorbable stents are also part of the device landscape, each with distinct clinical benefits depending on patient conditions.

By procedure type, PCI is segmented into primary PCI, elective PCI, and rescue PCI. Primary PCI is typically conducted during acute myocardial infarction and is known for delivering improved patient outcomes. Elective PCI is scheduled in stable patients with diagnosed coronary artery disease, while rescue PCI is performed following a failed thrombolysis.

In terms of end-users, hospitals hold the largest market share, owing to their well-equipped infrastructure and availability of skilled cardiologists. Ambulatory surgical centers and specialty cardiac centers are also emerging as notable end-user segments due to their growing preference among patients for cost-effective and quicker treatments.

Industry Latest News

Recent developments in the Percutaneous Coronary Intervention market reflect the industry's dynamic nature. Key industry players are continuously focusing on R&D investments to bring next-generation devices into the market. Innovations in biodegradable stents and bioresorbable scaffolds are gaining momentum, with clinical trials showing promising results in terms of vascular healing and reduced long-term complications.

Robotics and artificial intelligence (AI) are also making inroads into interventional cardiology. Robotic-assisted PCI systems are gaining attention due to their potential to enhance precision, reduce radiation exposure to clinicians, and improve procedural outcomes. Furthermore, advanced intravascular imaging technologies such as Optical Coherence Tomography (OCT) and Intravascular Ultrasound (IVUS) are improving diagnosis and procedural planning, thereby increasing procedural success rates.

Mergers and acquisitions continue to play a pivotal role in shaping the competitive landscape. Strategic collaborations between medical device companies and healthcare institutions aim to enhance product portfolios, leverage complementary strengths, and expand geographical reach. Additionally, regulatory approvals for novel products are contributing to the expansion of PCI device offerings in emerging markets.

Key Companies

The Percutaneous Coronary Intervention market is characterized by the presence of several established and emerging players. Leading companies include:

-

Medtronic plc: Known for its wide range of stents and catheters, Medtronic continues to focus on innovation and market expansion through partnerships and acquisitions.

-

Abbott Laboratories: Abbott is a major player with its extensive portfolio of PCI devices, including the Xience series of drug-eluting stents, which are among the most widely used globally.

-

Boston Scientific Corporation: With strong global distribution and a robust R&D pipeline, Boston Scientific plays a key role in shaping market trends through the introduction of novel products.

-

Terumo Corporation: This Japanese company offers a range of interventional cardiology products and is expanding its footprint in both developed and emerging markets.

-

B. Braun Melsungen AG: Known for its cost-effective PCI solutions, B. Braun focuses on making advanced cardiac care more accessible, particularly in developing regions.

Other notable players include Cardinal Health, Biotronik, Cook Medical, and Siemens Healthineers, each contributing to the innovation and competitiveness of the market.

Market Drivers

Several factors are driving the growth of the Percutaneous Coronary Intervention market. The foremost is the global rise in cardiovascular disease prevalence, which remains the leading cause of death worldwide. The aging population further exacerbates this trend, as elderly individuals are more susceptible to coronary artery disease.

Technological advancements in stents, balloons, and catheter systems have made procedures safer and more effective, boosting confidence among healthcare professionals and patients. The growing adoption of minimally invasive techniques has significantly reduced hospitalization time, post-operative pain, and overall healthcare costs, making PCI a favorable option over traditional coronary artery bypass grafting (CABG).

Government initiatives and reimbursement support in developed countries are also fostering market growth. Efforts to improve healthcare infrastructure, especially in emerging economies, are making PCI procedures more accessible. Moreover, rising awareness about preventive cardiovascular care and early diagnosis is increasing the number of elective and routine PCI procedures.

Browse In-depth Market Research Report -

https://www.marketresearchfuture.com/reports/percutaneous-coronary-intervention-market-3166

Regional Insights

Regionally, the North American market leads in terms of revenue, primarily due to a high incidence of lifestyle-related cardiovascular diseases, well-established healthcare systems, and rapid adoption of innovative medical technologies. The United States, in particular, is a key contributor with robust R&D activity and a favorable regulatory environment.

Europe follows closely, with countries like Germany, France, and the UK investing heavily in modernizing cardiovascular treatment facilities. The presence of globally renowned research institutions and a high penetration of advanced stents and catheters enhance market performance in this region.

Asia-Pacific is emerging as a high-growth market due to increasing healthcare investments, a rising geriatric population, and growing awareness about heart health. Countries like China, India, and Japan are witnessing a surge in PCI procedures, supported by improved healthcare accessibility and favorable government policies.

Latin America and the Middle East & Africa are also expected to show promising growth. While these regions are still developing in terms of healthcare infrastructure, increasing public and private investments and partnerships with global medical device companies are enhancing PCI accessibility.

Explore MRFR’s Related Ongoing Coverage In Healthcare Domain:

Comments

0 comment