US Cataract Surgery Device Marke Overview

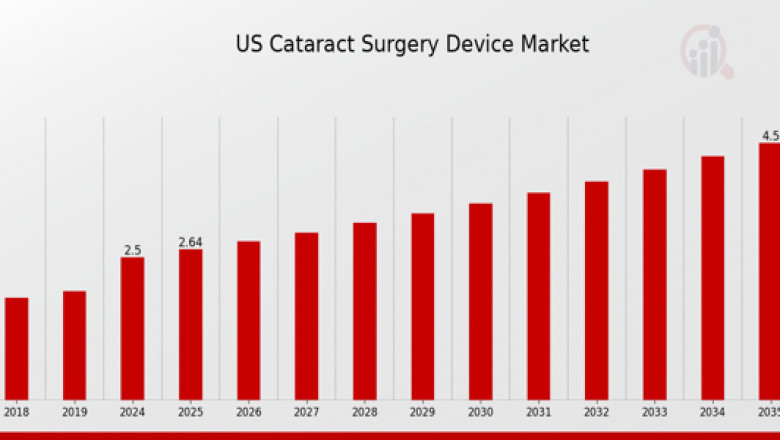

The US cataract surgery device market is witnessing notable growth due to the rising geriatric population, increasing prevalence of cataracts, and continuous advancements in surgical technologies. Cataract surgery is one of the most commonly performed procedures in the United States, with millions of operations taking place annually. The growing demand for minimally invasive procedures with rapid recovery and better visual outcomes is pushing the adoption of advanced surgical tools and devices. The market includes a broad range of devices such as intraocular lenses (IOLs), phacoemulsification machines, femtosecond lasers, viscoelastic devices, and other essential surgical accessories. With the increase in age-related eye disorders and improvements in healthcare access, the US market is positioned for sustained growth. US Cataract Surgery Device Market Industry is expected to grow from 2.5(USD Billion) in 2024 to 4.5 (USD Billion) by 2035.

The market is primarily segmented based on product type, end-use, and application. Among the product types, intraocular lenses (IOLs) dominate the market. IOLs are implanted into the eye during cataract surgery to replace the cloudy natural lens, and they are available in several variants including monofocal, multifocal, toric, and accommodative lenses. The adoption of premium IOLs is on the rise as patients seek enhanced post-surgical vision without dependence on glasses. Phacoemulsification equipment is another major segment, widely used for lens emulsification during cataract removal. Femtosecond lasers, although costlier, are gaining popularity due to their precision, safety, and ability to automate key steps in the surgery.

From an end-use perspective, hospitals hold the largest market share, owing to the presence of well-established surgical infrastructure and experienced ophthalmologists. Hospitals conduct a significant proportion of cataract procedures, especially for high-risk or complex cases. However, ambulatory surgical centers (ASCs) are rapidly gaining ground as they offer cost-effective and efficient services with shorter wait times and lower postoperative complication rates. ASCs now perform nearly one-third of cataract surgeries in the country. Ophthalmology clinics also serve a significant share of the market, particularly in urban and suburban areas.

The application segment is categorized based on the type of cataract being treated. Posterior subcapsular cataracts, nuclear cataracts, and cortical cataracts are the primary types. Among these, posterior subcapsular cataracts contribute significantly to revenue due to their higher visual impact and faster progression, requiring earlier surgical intervention. The availability of advanced diagnostics and customized treatment options has enabled ophthalmologists to deliver more targeted and effective care to patients.

Recent industry developments are playing a key role in reshaping the market landscape. Intraocular lens technology has undergone significant transformation, with companies introducing lenses that improve contrast sensitivity, reduce glare, and offer extended depth of focus. For instance, newly launched IOLs now offer enhanced performance in low-light conditions and provide patients with clearer vision at varying distances. Laser-assisted cataract surgery is becoming increasingly common, driven by the benefits of greater precision and reproducibility. The integration of digital platforms and surgical visualization systems is also gaining traction, enabling real-time data analysis and surgical guidance for improved outcomes.

Key companies in the US cataract surgery device market are heavily investing in research and development to gain a competitive edge. Alcon, a leading eye care brand, has introduced various advanced products for cataract surgery including its next-generation phacoemulsification systems and high-performance IOLs. Johnson & Johnson Vision continues to innovate with its TECNIS line of IOLs and the VERITAS Vision System, offering high-end surgical precision and reduced energy use. Abbott Laboratories remains active in the laser cataract device space, leveraging its expertise in ophthalmology and diagnostics. Carl Zeiss Meditec AG focuses on combining imaging, digital integration, and surgical technologies to create a seamless cataract surgery experience.

Bausch & Lomb is expanding its portfolio through acquisitions and partnerships to offer a comprehensive range of surgical tools and lenses. STAAR Surgical and HOYA Corporation are also contributing to the market through premium lenses and surgical innovations. RxSight, a newer entrant, has gained attention with its FDA-approved Light Adjustable Lens (LAL) that allows post-operative vision adjustments using light-based customization—a groundbreaking solution for precise vision correction. These companies are also engaged in strategic collaborations and regional expansions to strengthen their market presence.

Browse In-depth Market Research Report -

https://www.marketresearchfuture.com/reports/us-cataract-surgery-device-market-13569

Several market drivers are accelerating the adoption of cataract surgery devices in the US. The most notable driver is the aging baby boomer population. As people age, the risk of developing cataracts increases substantially, creating a large patient pool that requires surgical intervention. Additionally, increased awareness of eye health and early diagnosis has led to more people seeking cataract surgery earlier in the disease progression. Technological advancements in both surgical techniques and devices have also made the procedure safer, faster, and more effective, enhancing patient satisfaction and encouraging elective surgery.

Insurance coverage and favorable reimbursement policies play a crucial role in expanding the accessibility of cataract surgeries. Medicare and private insurers provide partial or full coverage for standard cataract procedures, and there is growing interest in premium IOLs despite out-of-pocket costs. The increasing number of outpatient facilities and ASCs is also expanding service availability in non-urban areas, improving geographic access to care. Lastly, improvements in teleophthalmology and electronic medical record integration are supporting better pre-operative assessments and post-operative care, streamlining the entire surgical process.

Regionally, the demand for cataract surgery devices varies across the US. States with a higher proportion of elderly populations such as Florida, Arizona, and California represent major markets due to higher surgical volumes. Urban centers with advanced medical facilities and teaching hospitals also report high adoption rates of the latest technologies. On the other hand, rural areas are increasingly benefitting from mobile surgery units and expanded access to ASCs, which help bridge gaps in specialized care delivery. Federal initiatives to support rural health infrastructure are expected to further aid in the penetration of cataract treatment services.

Comments

0 comment